The rising costs of tuition and mounting student loan debt loans for American students have become an understandable focus of this round of presidential hopefuls.

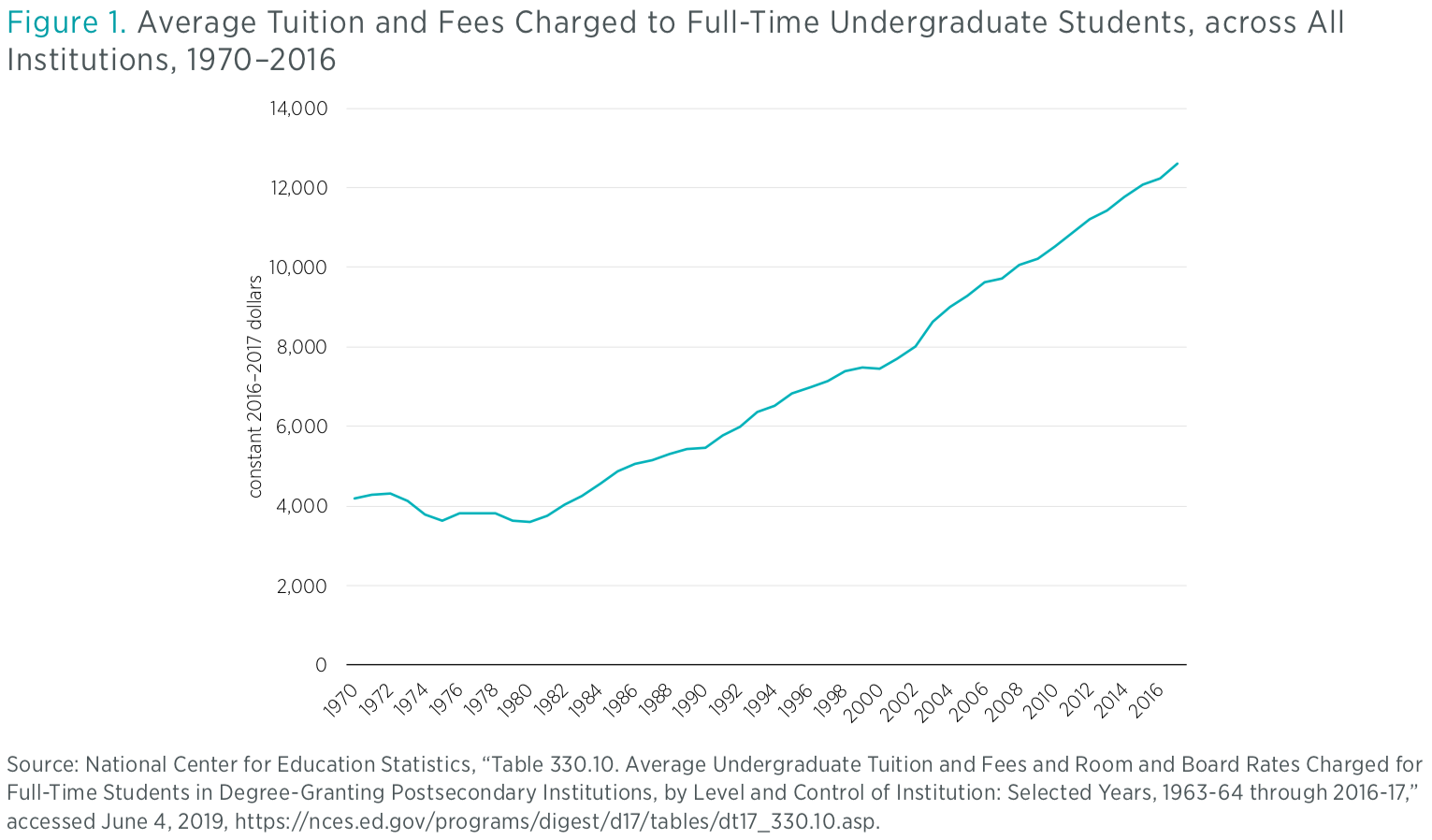

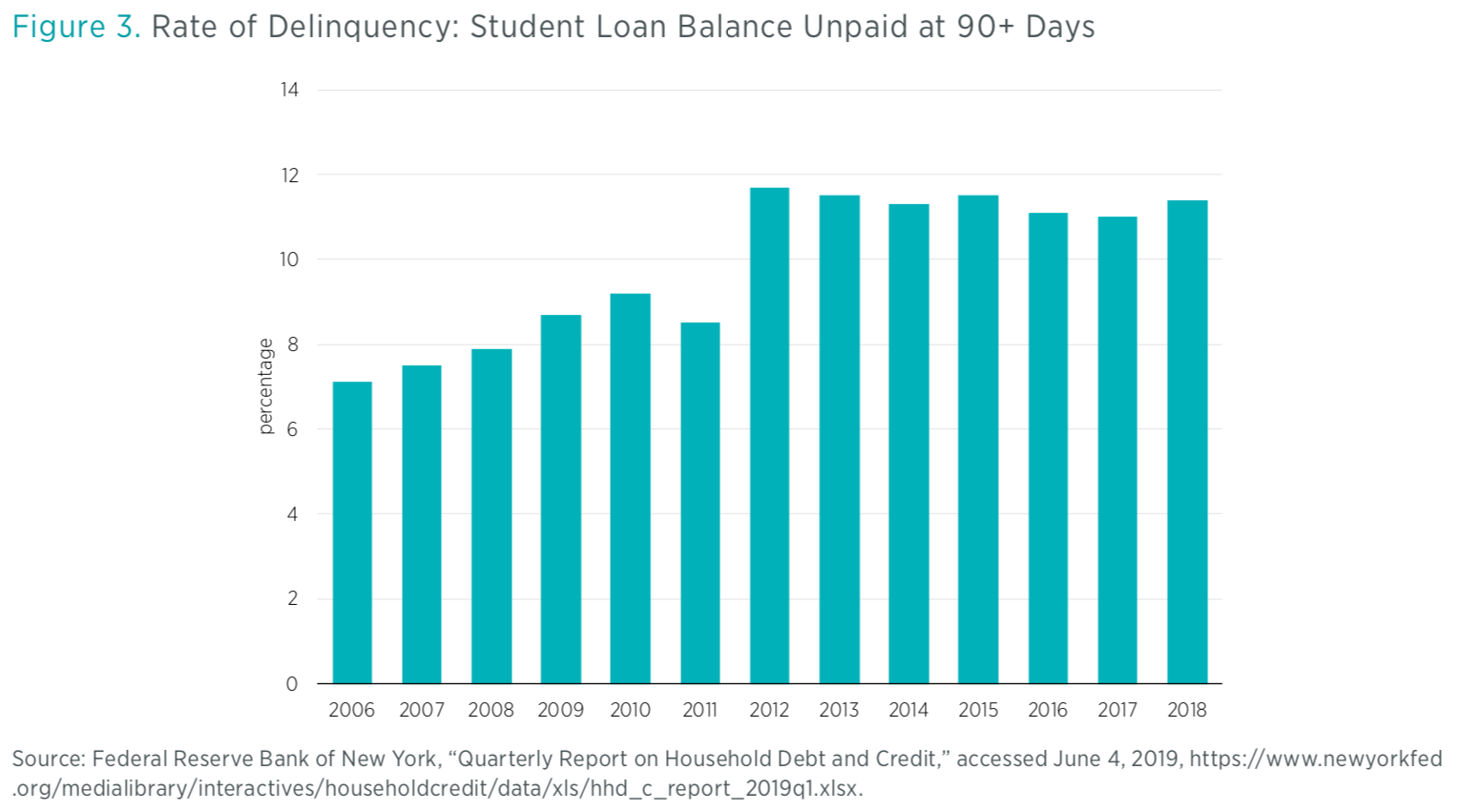

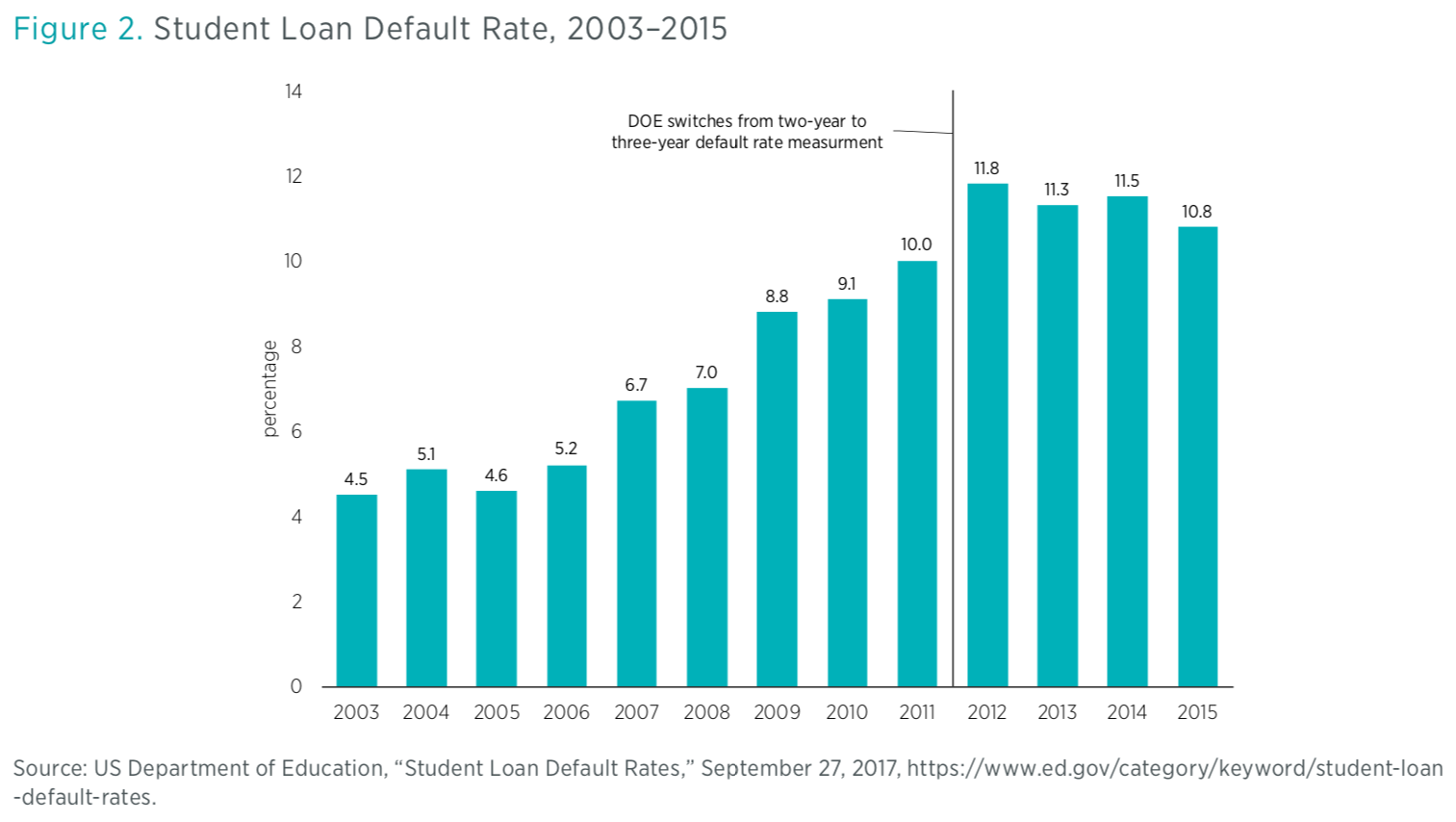

The average cost of tuition and fees for full-time undergraduate students has tripledfrom around $4,000 a year in 1970 to well over $12,000 a year in 2016. The Federal Reserve estimates that outstanding student loan debt is around $1.48 trillion. Unsurprisingly, students have struggled to pay these staggering costs, with roughly 20 percent of student loans either delinquent or in default by 2018.

Clearly, this is a serious problem that demands a serious response. Unfortunately, many of the proposals put out so far could merely make the situation worse. For example, most of the Democratic candidates support expanding the Pell Grant program to include more recipients with more federal funding.

A new policy brief by Mercatus senior research fellow Veronique de Rugy and research assistant Jack Salmon examines the nuances of federal higher education funding to understand the effect that such proposals could have on overall education affordability and access. They find that doubling down on the policies that got us here will have a predictable result. To address the higher education cost problem head on, policymakers should avoid and reform policies that lead to increases in tuition and therefore debt.

When “Affordability” Isn’t Affordable

Why have college prices skyrocketed since the 1970s and 1980s? Ironically, policies meant to expand higher education affordability have had the adverse effect of making it less affordable for everyone.

De Rugy and Salmon discuss how federal higher education policy notably changed with the passage of the Middle Income Student Assistance Act in 1978. This bill “expanded eligibility for federally subsidized loans to all undergraduate students, regardless of financial need, and expanded eligibility for Pell Grants to middle-income students.” Pell Grants were further extended in the 1980s, and in the 1990s several other federal financing options became available. Government aid to higher education expanded from a mere $3 billion in 1970 to an astounding $160 billion in 2017.

This steady increase of government aid to higher education is mirrored in rising tuition costs and nearly insurmountable debt loads over the same period. It is true that many people used these programs to attend college over this time. But this “assistance” came at a high cost in the form of unbearable tuition hikes. These policies have ensured that the debt burden for today’s students is far greater than in any era in history.

Former Secretary of Education William J. Bennett wrote way back in 1987 that while financial aid may benefit students in the short-term, federal loans and grants affect the economic gears behind tuition in subtle ways.

Unfortunately, educational institutions react to federal loans in ways that disadvantage students. Instead of allowing students to attend college at the discounted rate after government subsidies, colleges use these subsidies to charge a higher tuition overall. The artificial stimulus inevitably leads to higher tuition prices overall, giving the illusion of tax-funded benefit in the short-term and increasing the burden of loans in the long-term.

This is not the only adverse effect of government-subsidized tuition. Universities disbursing federal aid often use the overall rise in tuition to increase prestige, lowering the price of school on the surface and thereby increasing demand. This leads to more competition, which eventually pushes out lower-income students, canceling out any “good” that student loan supporters purport.

Many studies have empirically corroborated Bennett’s thesis. Bradley Curs and Luciana Dar measure the changing of net prices in state financial aid policy and determine that overall tuition prices are lower when states increase merit-based aid over loans. Stephanie Cellini and Claudia Goldin contribute to the Bennett hypothesis even further with their findings on federal aid programs versus for-profit trainings, finding that students opt for the latter when the former prove too rigorous.

As de Rugy and Salmon conclude, “the evidence broadly suggests that institutions of higher education are capturing need-based federal aid.” The overall effect of federal student aid may have generated up to a 102 percent increase in tuition from 1987 to 2010.

Better Ways to Onboard Students

The past decades of experience with federal student loan programs shows they have been a well-intentioned but ultimately self-defeating failure. Rather than expanding higher education access to those who otherwise could not afford to attend college, federal loan and grant programs have made a university education more expensive for everyone.

Proposals to expand upon these policies will only make the problem worse. This is not to say there is nothing that can be done about higher education affordability. First, the federal programs that have led to runaway higher education costs should be reformed or disbanded.

Next, de Rugy and Salmon discuss alternative measures like institutional aid, which have empirically been found to expand access without increasing tuition costs or taxpayer liabilities. Institutional aid consists of grants which never need to be paid back, come at no cost to the tax-payer, and are awarded based entirely on merit, leaving room for students from all socioeconomic backgrounds. Perhaps this kind of aid would become more attractive in the absence of federal grant and loan programs.

Finally, the authors suggest that these federal programs may have had the adverse effect of encouraging young Americans to pursue a college education when vocational school or on-the-job training and apprenticeships may have truly been a better fit for them. Our population is diverse, with diverse skills and aims, and our educational policies should reflect that. Policymakers should consider how our laws encourage or discourage such pursuits, and amend them accordingly.

{kind=link}

{kind=link}

{kind=link}